Moldova’s Productivity Trap: Why Good Firms Can’t Grow

Editorial Note: This article is written by Mihnea Constantinescu, Deputy Governor of the National Bank of Moldova, as part of Moldova Matter’s new series “The Next Economy: Moldova 2030.”

Disclaimer: The views expressed in this document are of the author and do not necessarily represent those of the National Bank of Moldova.

Moldova’s economy faces a persistent puzzle. Entrepreneurs start businesses regularly. In a good year, agricultural exports flow steadily. Yet the country’s productivity growth lags far behind its European neighbors. The problem is not lack of ambition, it’s that firms enter small and stay small, do not innovate and only rarely are able to cover the fixed costs of internationalization. Given the small internal market size, exporting is the most likely growth source. Several concrete mechanisms trap enterprises in low-productivity equilibrium, regardless of how hard entrepreneurs work or how good their business ideas might be. Lack of credit is only one part of the answer.

The Information Problem: When Nobody Knows Who’s Creditworthy

At the heart of Moldova’s growth constraint lies a fundamental information asymmetry. Banks need to know: Is this borrower reliable? Will they repay? What assets can secure the loan if things go wrong? In developed economies, these questions get answered through comprehensive credit bureaus, transparent financial statements, and enforceable collateral registries. In Moldova, these information channels are either broken or non-existent.

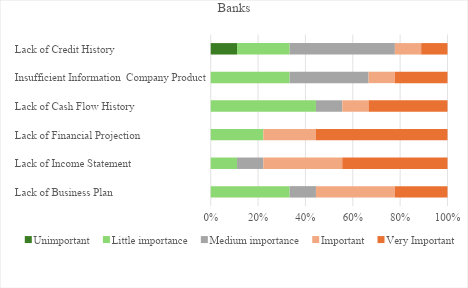

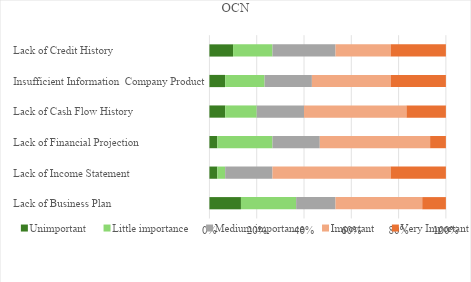

My survey of Moldova’s financial institutions (Constantinescu (2025)1) reveals how this plays out in practice. Survey participants, nine commercial banks and 54 non-bank credit organizations (OCNs), indicate they operate in essentially different markets. Not by choice, but because they are responding rationally to different information environments.

Banks concentrate on firms that can provide detailed documentation: 78% consider comprehensive financial statements critical for lending decisions, and 89% rate real estate collateral as very important. When you can’t easily verify a firm’s payment history, operational capabilities, or growth prospects, you default to what you can see and measure: buildings you can seize if the loan goes bad, and audited accounts that external professionals have verified.

OCNs occupy the space banks will not touch, functionally and geographically. Nearly half (48%) rely heavily on personal guarantees from business owners—essentially betting on the individual rather than the business. They evaluate firms through holistic assessments that incorporate “soft” information: most likely

...This excerpt is provided for preview purposes. Full article content is available on the original publication.