Time to Pump the Brakes on Artificial Intelligence Finance?

Deep Dives

Explore related topics with these Wikipedia articles, rewritten for enjoyable reading:

-

Dot-com bubble

15 min read

The article draws parallels between current AI investment mania and historical tech bubbles. Understanding the dot-com bubble's mechanics—circular investments, inflated valuations, and eventual collapse—provides essential context for evaluating whether AI financing follows similar patterns.

-

Special-purpose entity

11 min read

The article discusses SPVs like 'Beignet' being used to keep massive debt off corporate balance sheets. Understanding how these financial structures work, their legitimate uses, and their role in past financial crises (like Enron) illuminates the risks described.

-

Shadow banking system

17 min read

The article describes private credit, off-balance-sheet financing, and private equity firms funneling insurance assets into AI deals. This mirrors shadow banking dynamics that contributed to the 2008 crisis—understanding this system explains the systemic risk concerns raised.

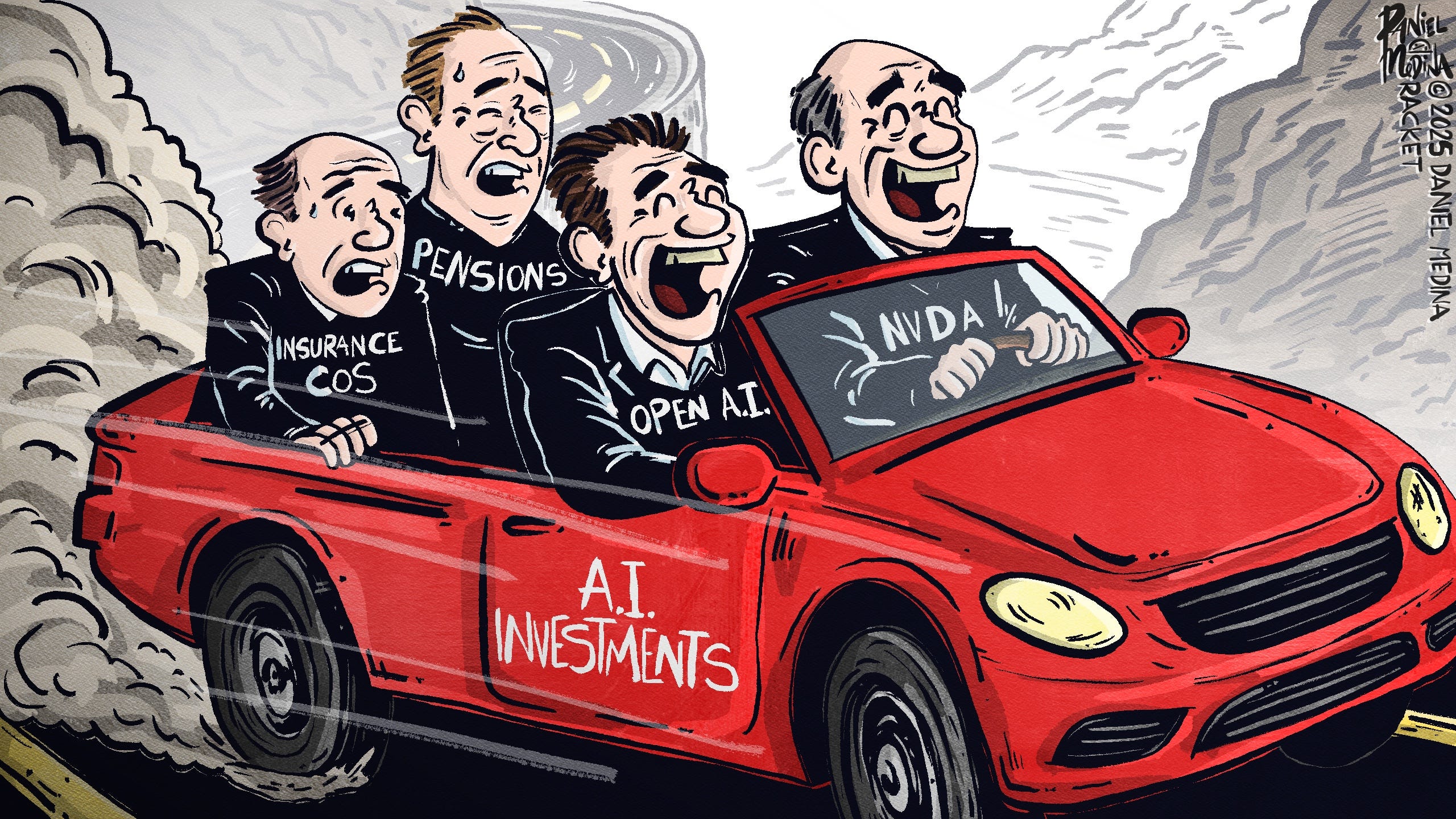

Artificial Intelligence dealmaking has surged in 2025 and looks to keep right on going in 2026 on the way to the stupidity where all booms eventually end up.

Deals among the major players have reached around $1 trillion. Nearly every week, tech giants like Oracle, Meta, Amazon, Microsoft, Google and Nvidia announce multi-billion dollar circular investment deals with AI, large language models, or “chatbot” creators such as OpenAI, Anthropic, and xAI, along with data center providers like Coreweave and several smaller firms. These are circular investments where the tech giants pour billions into AI chatbot companies, which rely on massive data centers and purchase or lease millions of graphic processing units (GPUs), the chips used for AI computing.

Amazingly, the deals closed in 2025 may be just the tip of the iceberg. A recent study by McKinsey & Co. concluded that data centers will require $6.7 trillion worldwide to keep pace with demand for computing power.

What could go wrong?

Concerns for hyperscaler stock investors

Hyperscalers provide large cloud-based computing services, the largest being Microsoft, Oracle, Meta, Amazon and Google. Institutional investors, including pension funds and insurance company portfolios, own large amounts of hyperscaler stocks. The tremendous and historic capital expenditures (“CapEx”) by hyperscalers could significantly weaken the financial position of companies that make up 26.1% of the S&P 500 as of November 26th. The spend now and expect revenues to catch up in 3 to 5 years plan is a perilous and perhaps fanciful proposition. Revenue is dependent on the success of the leading chatbot developers, the biggest being OpenAI. Fortune Magazine recently reported that investment bank HSBC doesn’t expect OpenAI to deliver profits that soon

HSBC Global Investment Research projects that OpenAI still won’t be profitable by 2030, even though its consumer base will grow by that point to comprise some 44% of the world’s adult population (up from 10% in 2025). Beyond that, it will need at least another $207 billion of compute to keep up with its growth plans. This stark assessment reflects soaring infrastructure costs, heightened competition, and an AI market that is surging in demand and cash-intensive to a degree beyond any technology trend in history.

Additionally, the AI ecosystem of hyperscalers, chatbot creators and AI chip makers is incredibly integrated.

This inter-connectivity could lead to a systemic meltdown as the problem of one major player could become

...This excerpt is provided for preview purposes. Full article content is available on the original publication.